Epixel Watch: Financial Health Insights

Epixel Watch: Financial Health Insights

Businesses cannot function smoothly if there is a blockade in their workflow or cash flow, the latter more serious. Advanced technology platforms can make workflows efficient, but cash flow efficiency depends on identifying where the capital is trapped and taking smarter steps to release it for timely use.

In direct selling, the capital goes through different stages. Procuring raw materials, manufacturing products, stocking up inventory, finding distributors, and finally when the product reaches the customers, companies still can’t be sure if they are going to receive the cash until the return window is over. Amid these uncertainties, working capital gets trapped in unidentified corners, in unsold inventory, outstanding distributor payments, or pending commissions and hampers the ability of the company to invest in growth.

The Cash Conversion Cycle (CCC) shows how many days the capital is tied up in this loop of product manufacturing to final sale. In this article, through the CCC metric and a stress tool based on Monte Carlo simulation method, let us analyze possible scenarios and solutions for building an efficient Cash Conversion Cycle.

Cash Conversion Cycle = Days Inventory Outstanding (DIO) + Days Sales Outstanding (DSO) − Days Payables Outstanding (DPO)

The Monte Carlo simulation method will help identify the impact of sudden changes like drop in demand, delayed payments, or commission policy changes affecting the company’s cash flow. An action plan in as short as six steps will help reduce the length of the CCC and release cash that can be reinvested where necessary.

The Cash Conversion Cycle is now a boardroom agenda

CCC has grown in importance and has occupied a quiet yet notable place in business growth strategies. It is not a finance team’s metric anymore because it has now a strategic issue that needs the CEO, CFO, and board members’ attention. It directly impacts the survival, profits, and investor confidence of a company.

The direct selling industry is growing at a minimum of 5% annually since 2020 and is expected to reach $75 billion by the end of 2025.

IBISWorld

Today, most companies buy goods well in advance to prepare for upcoming seasons and market demands. They pay out customers earlier than they should to win their trust and keep them motivated. But cash from customers arrives really late to make up for the trapped capital period.

Interest rates keep increasing and companies have to bear the burden due to cash being locked in inventory, commissions, or customer purchases. This does not look appealing at all to investors because they look at companies with better cash flow than growth. This brings direct selling companies under pressure to fix their cash flow model.

A recent data insight by JP Morgan Chase found that a company that can reduce its CCC by 15 days can free up 6-10% of its annual revenue.

Direct selling companies earn an impressive EBITDA margin of 7-9% yearly. This combined with CCC improvements that release 6-10% cash equals an entire year of profit. And, this makes CCC the most important metric requiring the attention of C-level executives.

The basics of CCC challenges in direct selling

The basic concept of CCC is described mostly with reference to retailers, manufacturers, and wholesale distributors but in direct selling the case is different because of two unique factors.

Distributed inventory

Direct selling companies stock products in warehouses. Sometimes, multiple warehouses across countries. This is managed by a central system and doesn’t create much of a concern. But distributors also keep their own inventories and this creates real confusion as to where the inventory actually is and which part of these inventories contribute to Days Inventory Outstanding (DIO). As a result, DIO is underestimated.

Commission payout delays

Distributors are paid within 4-8 weeks before the company receives the cash. This process is within the CCC period and makes it more complex than it is for traditional consumer goods companies.

Days Inventory Outstanding (DIO)

Days Inventory Outstanding measures the number of days stocks sit in the inventory before being sold to the customer. Normal consumer goods companies keep a DIO below 60 days but direct selling companies especially the ones in beauty and wellness sectors tend to keep it longer than 90 days.

Companies in the beauty, wellness, and skincare industries manufacture products in small batches and these products take time before they are completely sold. They must keep a buffer batch and ensure that they do not expire before they reach the customer. Then there are items that only some distributors want, yet they have to produce and maintain stock levels so that distributors can access them any time.

All these factors cause the DIO to extend past 90 days and in some cases more than 120 days. When the products sit on the shelves without bringing cash, the company’s capital gets blocked without being able to allocate it for optimizing marketing campaigns, product development, or entering new markets.

Days Sales Outstanding (DSO)

Days Sales Outstanding calculates the number of days taken to collect the cash after a sale is completed. DSO has improved in recent years due to the use of digital wallets, autoship subscriptions, and real-time payment gateways. But even today, so many markets in Asia, Latin America, and the Middle East are still based on cash on delivery, offline banking and cheque clearing. The companies in these markets suffer from a slow cash in-flow, and DSO, at times, extends well beyond 40 days. Even an extra DSO stretch of five days traps cash which may amount roughly 1% of annual revenue.

Days Payables Outstanding (DPO)

Days Payables Outstanding is an estimation of the time a company takes to pay commissions to their distributors. The pay cycle design of direct selling companies vary, some may choose to pay their distributors on order completion and some others on their agreed organizational pay cycle which can take a month or later, or until a return window closes. There are companies who are lenient with early distributor payments when they have a healthy cash flow.

Extending DPO by 15 days is usually better than reducing inventory by the same amount because it is easier than adjusting the supply chain. But, over extension of payout can result in strained distributor-brand relationships, delayed shipments and eventually it casts a shadow on customer experience.

Consider an example of a direct selling company with an estimated DIO of 95 days, DSO of 38 days, and DPO of 42 days. The CCC for this company will be:

CCC = 95 (DIO) + 38 (DSO) – 42 (DPO) = 91 days

This means that it takes 91 days, almost a quarter, for every penny invested in operations to return to the company as cash. And this puts companies in a hard time because they have to respond to the rising and fading trends, distributor support, and investor confidence. A slower CCC will negatively impact all of these.

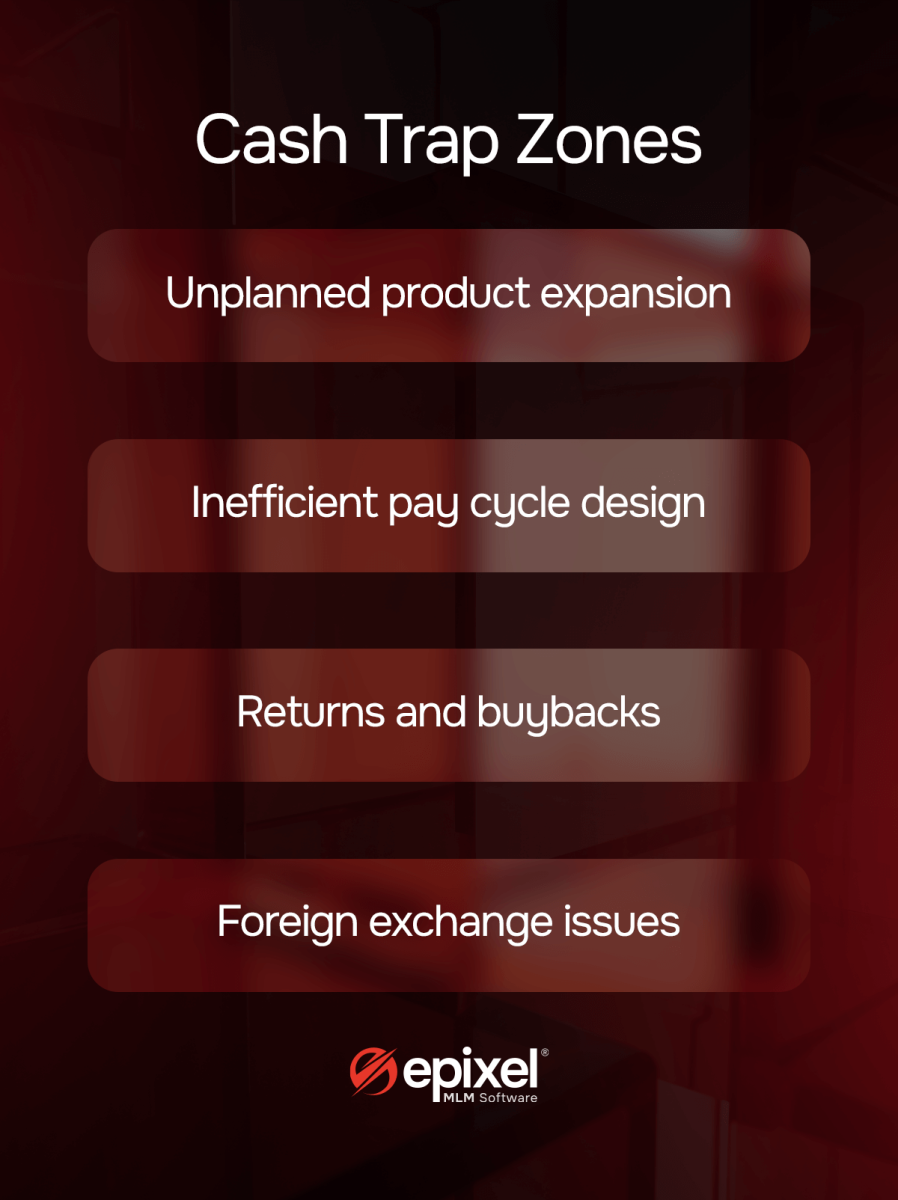

The cash traps inside direct selling operations

The working capital, big or small, can get stuck anywhere inside your operations. These little cash traps can slowly stretch your Cash Conversion Cycle without showing up on your dashboard. You will only know when the impact becomes so hard that you cannot ignore.

Unplanned product expansion

Top leaders and distributors demand brands to launch new product variations for each season or an upcoming trend. Companies in a haste to underline their market presence release products without a second thought. But, in the background what happens is companies have to either buy raw materials in bulk or products in minimum order quantities from the manufacturer to meet the unexpected demand. And when the demand turns out not as expected, the products pile up in the warehouse and with top distributors.

The problem was cited in a 2025 Bain study which revealed that SKU units increased inventory value, but the company revenue only grew by 14% which means that the company’s cash got trapped in inventory lengthening their CCC.

Inefficient pay cycle design

Setting just one pay cycle for all markets may not work well, especially when you have a list of international markets where cash payments and traditional bank transfers still pay a sale. But still, distributors in these markets expect brands to pay commissions just after closing a sale but brands could not decide otherwise for the fear of losing the market. In such cases, when companies pay distributors before the payment of the sale comes in, it creates a trap where cash sits with the distributor before he qualifies for it.

Companies with a weekly pay cycle, the commission liability can grow to more than 1.5 pay cycles.

This means that the company is paying its distributors from their working capital, and it is risky when there is a sudden increase in customer demand or other operational needs.

Product returns and buybacks

Meeting FTC regulations or similar consumer protection laws in different regions put direct selling companies under pressure to buy back the unsold inventory for up to 90 days. Distributors can return slow moving or hard to sell products back, and the company must take them back as the industry regulations mandate. But these returned products come back very close to expiry or in a packaging that cannot be resold at full value. This goes back into the warehouse and may not see an exit at all because it holds a high probability of being classified as a write-off.

The company suffers a double hit because they have to refund the distributor, and the returned product never sells. This makes returns and buy backs one of the costliest capital black holes.

Foreign exchange issues

Exchange rates and currency fluctuations create real challenges for internationally operating direct selling companies. Collecting revenue in one currency and paying out in another cause delays because cash moves through multiple payment methods like international clearing systems and fintech partners. Also, the companies lose around 2% while transacting in less common currencies.

The time it takes to convert cash into foreign bank accounts can increase DSO and the company cannot use the cash for domestic operations. Distributors, reluctant to bear the currency fluctuation rates, expect the company to make their payments excluding the spread, costing the company a percentage of its working capital.

Stress-testing Cash Conversion Cycle with Monte Carlo simulations

One thing that most finance teams get wrong is conducting an assumption-based test with fixed numbers without considering the reality. The approach is simple but does not consider real-world challenges that may arise in due course. For example, finance teams may decide to cut down on DIO by 10 days thinking that it would improve revenue but when there is a sudden increase in demand, this strategy backfires.

Monte Carlo method

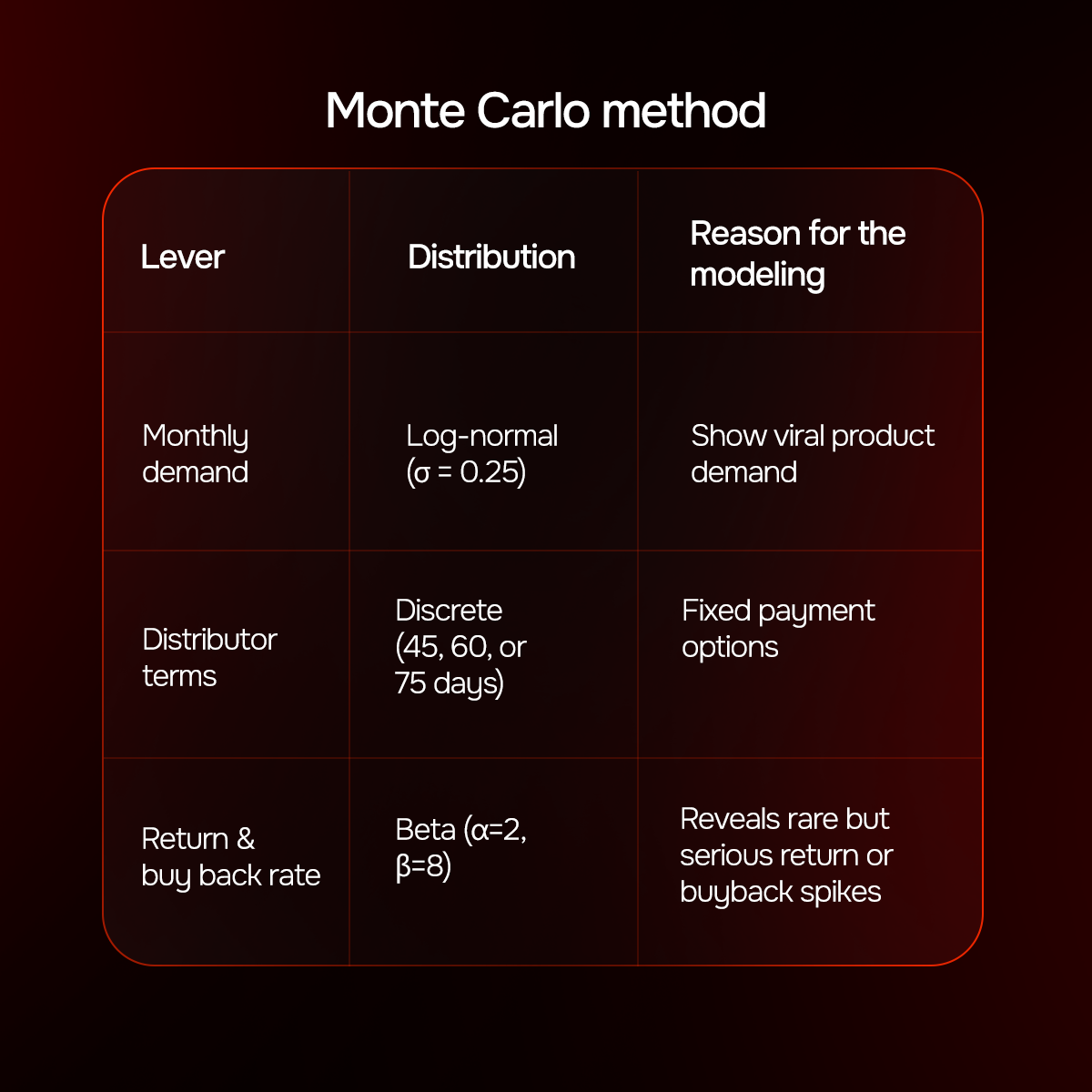

The Monte Carlo technique uses random sampling by taking into account the variabilities and uncertainties. DIO, DSO, and DPO are not random numbers in the Monte Carlo method. Possible variations that could happen across different business aspects are considered, and thousands of scenarios are run to generate a range of possible CCC numbers. With the Monte Carlo method, finance teams don’t get an average CCC but the probability of extreme variations that might happen.

The simulations also calculate various worst case scenarios to determine the extremes. Like, for example, your average CCC after calculation is 88 days but the Monte Carlo model could tell you that in 1 out of 10 scenarios, it can as well extend up to 121 days. It uses a realistic range of probabilities than a single value. A log-normal pattern is used to analyze monthly demand because sales normally are stable but can suddenly increase when a product goes viral. Distributor payment cycles always follow a fixed pattern, either 30, 45, 60, or 75 days. There aren’t many uncertainties and simulations pick one of these fixed distributions.

For return rate calculation, beta distribution is used with a percentage range (0-100%) because in this scenario, the chances for sudden spikes are low. The beta distribution also fits a policy change, bad batch, or market hits that end up in a sudden surge.

Monte Carlo simulations help finance teams see the worst 5-10% of situations so that the company does not end up witnessing “liquidity cliff months”.

Download a free Liquidity Stress Tool

Our Liquidity Stress tool, built with Google Sheets and Python Notebook calculates your Cash Conversion Cycle through inputs such as inventory details of each product, sales forecasts by country, distributor terms, and commission payout timing.

When the inputs are received, the tool generates three reports.

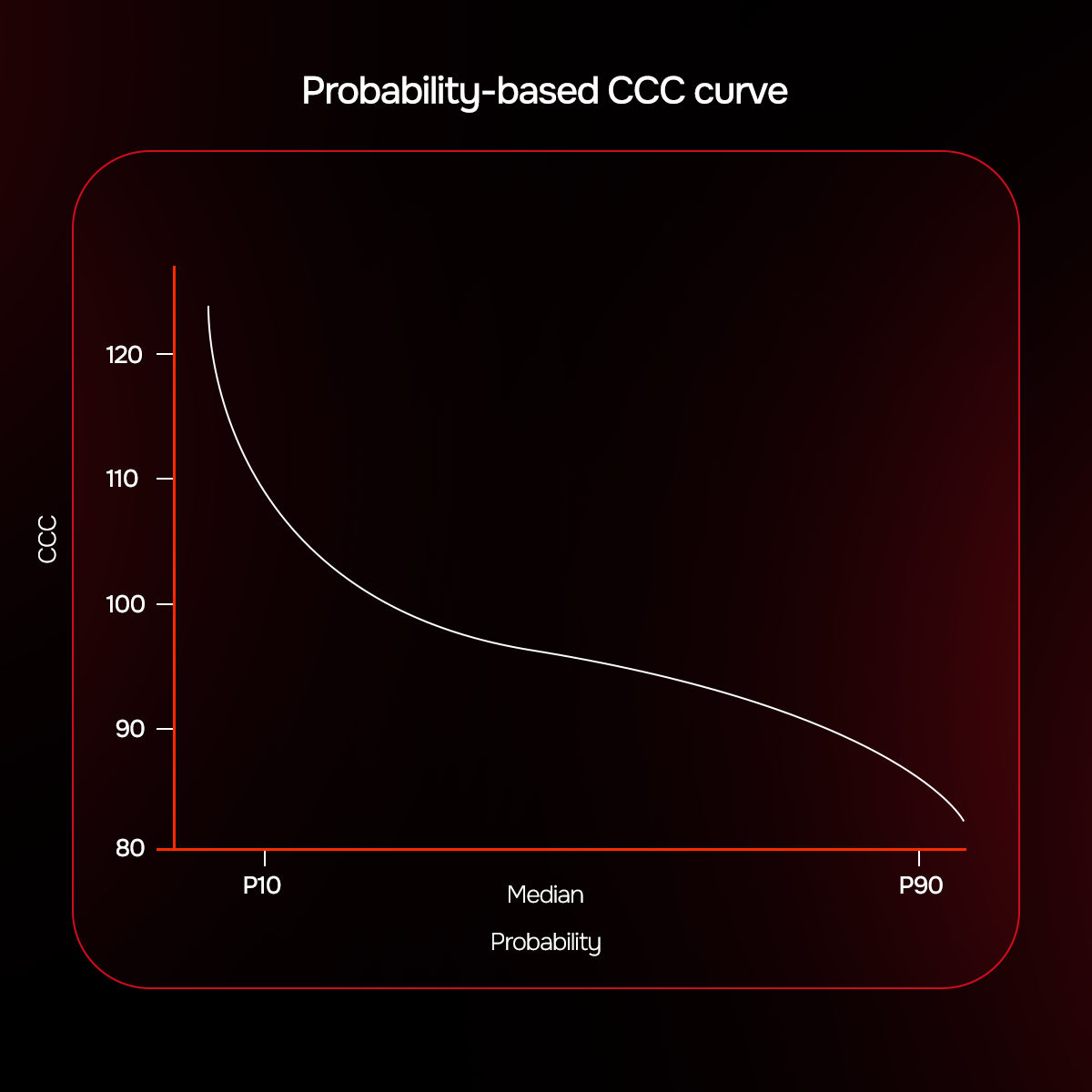

1. Probability-based CCC curve

The curve shows CCC as multiple scores from the best case (P10) to the worst case (P90).

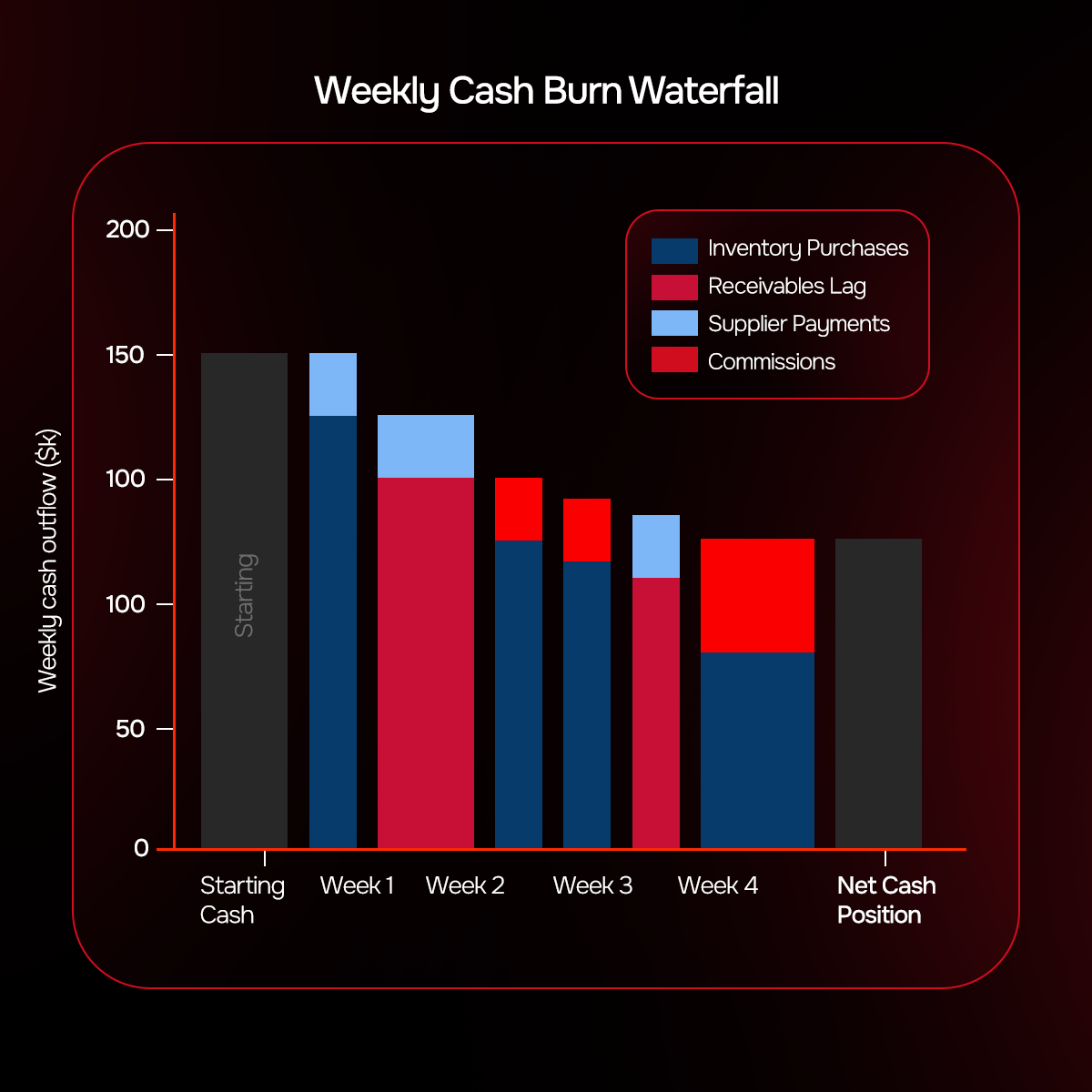

2. Cash-burn waterfall chart

This calculates how much cash goes out every week for buying inventory, waiting for receivables, and for paying suppliers and distributor commissions.

3. Early warning dashboard

It alerts the designated teams when cash forecasts go below the set limit.

Reduce your cash flow risks and forecast your Cash Conversion Cycle health with our Liquidity Stress Tool

Seven strategic methods to control CCC

Adopting these methods can improve the health of your Cash Conversion by reducing DIO, DSO, or extending DPO. This would compress the CCC by 20-35 days in 12 months for inventory-based businesses like direct selling.

Lock-in your safety stock

Instead of keeping inventory for 12 weeks, segment products in groups of A, B, C based on their value with strict reorder points. This reduces excess stock and improves DIO by 5-12 days but carries a risk of stock running out on hero products if their demand increases.

Integrate demand data from all channels

Pull real-time insights from TikTok, Shopify, and other channels for AI-driven demand forecasts. This can reduce DIO by 7 days by predicting products in demand, however, demand surges can happen through influencer promotions.

Put distributor payout on hold

Instead of paying distributors upfront, companies can hold their payouts in escrow wallets until the customer's payment is successful. This improves Cash Conversion Cycle by 4-6 days because you are not paying them from your capital reserve. Distributors might feel insecure about their delayed payouts if not properly communicated.

Approach invoice-financing marketplaces

You can receive 70-90% of your approved customer invoice from invoice-financing marketplaces like Fundbox or Tipalti at 1-3% discount. This cuts DSO by 5-15 days and ensures there are no financial crunches for the company. What is to be considered is that the discounts are not costlier than your capital.

Supplier reverse factoring

Partner with banks to pay your suppliers on time for low interest rates and you repay the bank when cash comes in. This improves supplier relationship and adds 8-18 days to your DPO. This can only be availed if you have a strong credit score.

Sell on returns auction platform

Products that are close to expiry date or returned products can be auctioned to liquidators via flash sales. This reduces DIO by 2-5 days but white label the products to protect your brand integrity.

Restrict distributor inventory buy backs

Distributor inventory coming back after 30 days may not be taken in full. You can set up buyback policies at 80% but ensure compliance in markets with stricter consumer protection policies. This can reduce DIO by 3-6 days and discourages over ordering.

Preventing perverse incentives that harm Cash Conversion Cycle

Perverse incentives are rewards tied to wrong outcomes like distributors paid on invoiced sales not received cash or promoted to higher ranks for just placing orders.

Balanced scorecards for Country General Managers

Country Managers should be given two goals together, growth target and liquidity target. Growth target in relation to sales, new customers, and market share, and liquidity target to improve CCC. Because giving only CCC as the target can result in the application of wrong strategies like cutting marketing, limiting stock, or delaying distributor payouts that can affect growth at large.

Fixed vs floating commissions

Never link higher commissions on invoiced sales and introduce bonus for cash collected from customers. If commissions are paid on invoiced sales, then there are chances of distributors pushing products aggressively, creating channel stuffing, or placing fake orders which will never turn in cash.

Quarterly risk drills

Leadership must simulate a series of what-if scenarios every quarter like

- A sudden 20% drop in demand

- A 30-day shipping delay

- A supplier disruption

- A spike in returns or credit chargebacks

This can be done using Monte Carlo simulations. It gives you the chance to practice responses before a real crisis hits.

Action plan for improving the Cash Conversion Cycle

- Recalculate CCC for the last six quarters with commission payout lag included.

- Identify cash traps with a swim-lane diagram that shows how cash moves through inventory, receivables, payables, and distributor payouts.

- Deploy the stress-test tool with next year’s budget input and run 10,000 Monte Carlo simulations to understand uncertainties and flag P90 cash troughs.

- Choose two methods that unlock liquidity faster, like supplier reverse factoring and safety stock segmentation.

- Redesign distributor policies like selecting an escrow wallet or linking bonuses to collected cash not invoiced sales. Test this in one region before implementing it across all markets.

- Link CCC KPIs into OKRs (Objectives and Key Results) of every department including supply chain, sales, and payouts that influence cash flow.

- CCC should be a mandatory topic on the quarterly board agenda just as EBITDA and revenue is.

Discover how we build resilient businesses with advanced MLM functionalities

Conclusion

Even minor cash traps can be like pitstops in a Formula 1 race. Every extra inventory in the warehouse or distributor hands or a commission paid earlier than it should be is costing companies valuable growth opportunities. The winners in 2026 are definitely not the ones that generate more sales, they are the ones that spin cash faster than their competitors to power expansion and innovation with their own capital.

Leave your comment

Fill up and remark your valuable comment.