Epixel Watch: Financial Health Insights

Epixel Watch: Financial Health Insights

When there is a glitch in payment, distributors get frustrated, customers lose trust, and the company will lose its reputation. For an MLM company, choosing the right payment strategy decides the future of your company. Most companies think payment channels are one-size-fits-all. They often go for the generic ones without analyzing what actually fits their specific business type and strategies.

This article intends to reduce all your confusion and lays out a detailed comparison of major payment gateways such as Stripe, PayPal, and customized payment channels. Whether you are new to the industry, an expanding brand or a company that wants to re-platform, the insights from this will help you take a decision that you won't regret in the long-term.

Why payment gateways are a strategic decision in MLM

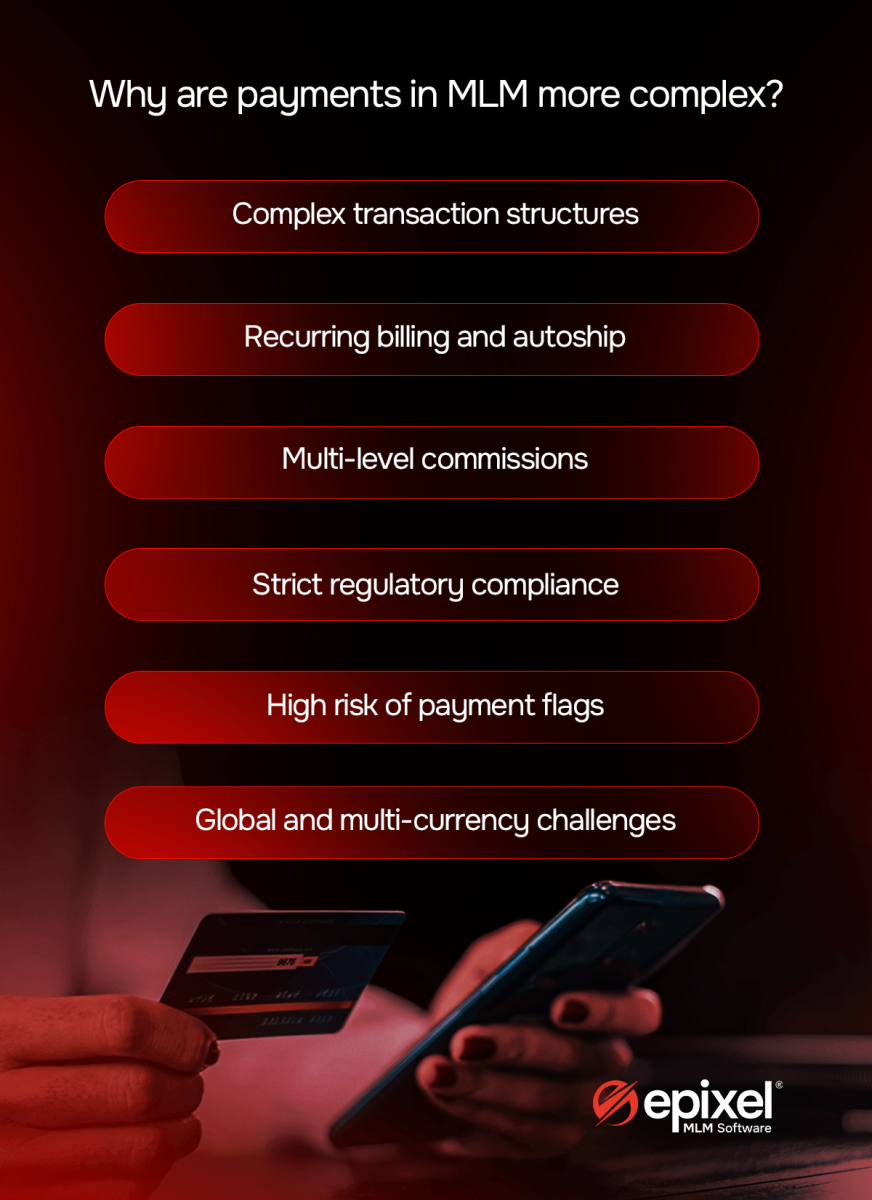

Before we get into the comparisons, it's important to know why payments in MLM are considered more complex than in e-commerce.

First, transaction procedures in MLM businesses come with a lot of complexity. Autoship billing, monthly subscriptions, product commissions, all run through the same infrastructure. During situations like a brand relaunch or rank advancements, transaction volumes can spike by 10x.

Second, MLM businesses operate under strict regulatory frameworks. Payment gateways may find this slightly riskier. So, activities like increases in chargeback rates can result in the payment channels blocking the transaction or stop partnering with the company altogether.

Although global expansion is an indication of growth, it complicates payments because operating in multiple countries involves multi-currency payout, local payment support systems, and country-specific compliance requirements.

With that said, we will take each of the options of payment infrastructure and compare them to draw a conclusion about what may be a potential fit for your type of business.

Stripe: The developer-friendly powerhouse

Stripe is definitely a fallback option for MLM firms that have very qualified technical operators. It is also flexible and has an API-based design, developers can tweak it without necessarily building the infrastructure from scratch. It is universally popular and this makes it attractive to large scale MLM firms with advanced software systems.

Where Stripe excels

Stripe is the best choice when it comes to handling complex billing procedures such as maintaining multi-tier autoships, prorated charges, failed payment retries, and automatic retry attempts when a card fails. For companies who have pricing based on different distributor ranks and sell different product bundles, a payment gateway that handles complex financial work will be beneficial.

Stripe Connect was a feature built for companies that had to split the amount amongst their users. Though it wasn't made exclusively for MLM companies, the features perfectly fit into the commission payout system used in MLM. Stripe Connect builds systems that route funds directly to bank accounts of distributors.

Stripe is one of the globally accepted payment third parties. It supports 135+ currencies, 40+ countries, and seamlessly integrates with many local payment methods across Europe and Asia Pacific. Hence, Stripe can be a suitable choice for companies planning to expand beyond North America.

Where Stripe falls short

The major drawback of using Stripe is that it has listed MLM as an elevated risk. It means it can terminate accounts without any detailed warnings. This won't give any time for companies to prepare for derisking, it will affect the revenue and strain cash flows.

Stripe can handle the regular payout split but it may fall short in handling commission dashboards, reconciliation systems and hold management. It's the responsibility of the technical team to build it. So, Stripe just provides the framework, the details must be designed and developed by the MLM company.

Stripe typically charges 2.9% of total amount as transaction fees. This is particularly not an issue for small scale companies. For large scale companies with annual sales of millions of dollars, the transaction fees act as an operating cost. Although payment processors provide discounts to large companies, it's not usual for Stripe to provide the same. Hence, it's wise for companies to have a direct relationship with the bank or have negotiated contracts.

Best fit: Stripe is recommended to companies with a technical team that has expertise in API integration, for companies in its growing stage where the annual sales revenue is between $1 million and $50 million. It is beneficial in the US or EU as Stripe has a strong infrastructure in those regions.

PayPal: The brand recognition play with hidden tradeoffs

PayPal has a reputation for providing safety to customers. This increases conversion rates as more people tend to check out faster when they see PayPal as an option. But like Stripe, PayPal also sees MLM as high risk, especially at the time of a volume spike. This may lead to the payment company holding or freezing the accounts, delaying the payment, and more.

Where PayPal excels

It's proven that PayPal plays a role in increasing conversion rates. This works mostly in Southeast Asia, parts of Latin America and some Eastern European markets as PayPal have become a household name. Even when the MLM company isn't popular enough, having PayPal as a choice of payment channel can earn trust among distributors and customers.

PayPal’s Venmo and PayPal balance is best for younger MLM brands and small scale distributors as these features don't involve intense bank procedures. MLM companies can directly pay into a PayPal wallet.

Where PayPal falls short

PayPal flags any business they consider fraudulent or resembles pyramid schemes. The complexity lies in what PayPal's internal risk team considers risky and how a compliant direct selling company functions. If their policies don't align with yours, it can lead to company accounts getting flagged. Now, this can cause unsteady cash flow and distributor distrust.

PayPal has a weaker API capability. It can't perform activities that have complexities in commission routing, multi-tier split and subscription customizations. Adding to the complexity, if the developers are not experienced enough to materialize the concept into code, large scale companies will have a difficult time handling PayPal.

PayPal has a bias for buyers, especially at the time of disputes. This can disrupt distributor trust and result in sudden quitting.

Who can use PayPal seamlessly? Larger companies can use PayPal as a secondary channel. It can be a suitable choice for MLM companies under $500k in annual sales who need a simple setup.

Custom payment solutions: The enterprise play

Payment gets complex as the company grows and reaches $20 million annual sales while operating across 10+ countries. It will become relatively difficult for simpler payment systems like PayPal and Stripe to handle this level of layered complexity. That's when customized payment channels become necessary.

Custom solutions can be done in two ways. The first way is to partner with banks in a specific region that can process payments from that region. The process will be done by a payment system developed by your own company. This is called direct merchant account combined with payment orchestration. On the other hand, some companies use in-house payment systems where all the payment procedures are done by the payment system built by the company and the weekly or monthly payout will be credited to the distributors’ bank account. In this case, no third-party banks will be involved in committing the payouts to distributors. MLM software like Epixel helps companies which can't build their own in-house system by providing MLM-specific payment modules.

Where custom solutions excel

When you don't have a third-party payment channel like Stripe or PayPal, the MLM company will have complete control over processing the payment, how many refunds and payouts a day. When a payment system is outsourced, the external payment gateway has the primary control and may take severe actions if they suspect an unusual number of payments from or toward the company. For a large MLM company handling payments worth millions a day, a small disruption in the payment channel can cause a huge amount of loss.

As we discussed earlier customizing allows payment orchestration. The payment system will direct the transaction to the suitable processor according to different situations. If one processor doesn't work, it redirects to another. Through this, retention increases as autoship operates properly with the help of this type of multi-rail payment system.

MLM companies often must pay distributors across the globe. Each country or region has different payment systems. A custom payment system integrates seamlessly with all payment rails.

In most regions, distributors are treated as independent contractors. Hence the companies are expected to generate tax forms. Payment systems like PayPal or Stripe often fail to do this as they only handle the job of processing the payment. While custom payment systems have features to process tax and auditing history.

Where custom solutions fall short

Custom payment solutions aren't as easy as they look from outside. Laying the infrastructure of a custom payment system is expensive. The cost includes payment gateway integrations, payout systems for distributors, security infrastructure, compliance systems, and payment orchestration software. This is not feasible for small scale MLM companies unlike in the case of large scale MLM that has a more than enough annual turnover.

Built-in payment systems like Stripe or PayPal may only take a few hours to start operating while a custom system can take months. The difficulty in handling compliance is real when it’s custom payments. One of the major requirements is to comply with PCI DSS. It's a global standard for companies that process credit card payments.

Building a custom payment system calls for an expert who knows how the infrastructure is laid and the operations run. Companies either need to have an in-house team or hire an external consultant for this purpose.

To summarize, custom payment systems work best for large scale MLM companies who have sufficient finance to afford the infrastructure and operations of a custom payment system.

MLM payment gateway comparison table

Below is a table that evaluates each payment gateway against important MLM components.

| Evaluation Criteria | Stripe | PayPal | Custom Solution |

|---|---|---|---|

| Setup and Onboarding | |||

| Setup Complexity | Low–Medium | Low | High |

| Time to Go Live | 1–2 weeks | 1–3 days | 3–12 months |

| Technical Skill Required | Medium–High | Low | Very High |

| Upfront Cost | $0–$5K | $0 | $50K–$500K+ |

| Transaction Fees | |||

| Standard Card Processing | 2.9% + $0.30 | 2.99% + $0.49 | 1.5%–2.2% (negotiated) |

| International Transactions | +1.5% | +1.5%–2.0% | Negotiable by region |

| Currency Conversion | +1.0% | +3.0%–4.0% | Negotiable |

| Volume Discounts | Enterprise only | Rarely | Yes — core advantage |

| Recurring Billing and Autoship | |||

| Autoship/Subscription Support | Excellent | Limited | Fully customizable |

| Dunning Management | Advanced | Basic | Custom logic |

| Failed Payment Retry Logic | Configurable | Minimal | Fully configurable |

| Billing Cycle Flexibility | High | Medium | Unlimited |

| Commission Payouts | |||

| Mass Payout Capability | Via Stripe Connect | Via PayPal Payouts | Multi-rail payout |

| ACH/Bank Transfer Payouts | US-focused | Limited countries | Global |

| Crypto/Digital Wallet Payouts | No | PayPal balance only | Configurable |

| Local Payment Method Payouts | Limited | Limited | Tipalti, Hyperwallet, etc. |

| Real-time Payout Option | Instant (fee applies) | Instant (fee applies) | Configurable |

| Global Operations | |||

| Currencies Supported | 135+ | 25+ | Unlimited (processor-dependent) |

| Countries for Processing | 46+ | 200+ (consumer) | Custom by region |

| Countries for Payouts | 40+ | 70+ | 200+ via partners |

| Local Payment Methods | Growing | Limited | Fully configurable |

| Multi-entity/Multi-country Support | Requires dev work | Complex | Native |

| Risk and Account Stability | |||

| MLM/Direct Selling Risk Classification | Elevated risk | High risk | Negotiated directly |

| Account Freeze/Termination Risk | Medium-High | High | Low (owned relationship) |

| Fund Hold Risk | Possible | Common | Minimal |

| Chargeback Threshold Tolerance | ~1% (strict) | <1% (very strict) | Negotiable |

| Dedicated Risk Manager Access | Enterprise only | Rarely | Standard |

| Compliance and Reporting | |||

| PCI DSS Compliance (managed) | SAQ A (merchant) | SAQ A (merchant) | SAQ D (merchant burden) |

| 1099/Tax Reporting Tools | Basic | Basic | Full automation |

| Audit Trail & Commission Records | API-accessible | Limited | Deep reporting |

| GDPR/CCPA Data Controls | Strong | Adequate | Fully configurable |

| DSA/FTC Compliance Features | Not MLM-specific | Not MLM-specific | Purpose-built options |

| Integration and Technical | |||

| API Quality & Documentation | Best-in-class | Adequate | Custom-built |

| MLM Platform Integrations | Widely supported | Widely supported | Native (if platform-built) |

| Payment Orchestration (multi-rail) | Single processor | Single processor | Core capability |

| Authorization Rate Optimization | Basic | Basic | Routing intelligence |

| Fraud Detection Tools | Stripe Radar | Built-in | Custom or third-party |

| Webhooks & Real-time Events | Excellent | Adequate | Custom |

| Distributor Experience | |||

| Consumer Brand Recognition | Growing | Very High | None (white-label) |

| Checkout Conversion Lift | Moderate | High (known markets) | Depends on UX build |

| Distributor Self-service Billing | Via portal | Via PayPal account | Custom portal |

| Mobile Checkout Optimization | Strong | Strong | Custom |

| Support | |||

| Support Quality | Email/docs-heavy | Notoriously poor | Dedicated account mgmt |

| 24/7 Support Availability | Enterprise only | Limited | SLA-driven |

| Dispute Resolution | Moderate | Buyer-favored | Direct bank relationship |

| Recommended for | |||

| Company Stage | Startup → Growth | Startup / Secondary option | Scale → Enterprise |

| Annual Sales Volume | $0 – $20M | $0 – $1M (primary) | $20M+ |

| Country Footprint | 1–5 countries | 1–3 countries | 5+ countries |

| Distributor Count | Up to ~50K | Up to ~10K | 50K+ |

Legend: Strong/Native capability | Limited or requires workaround | Not supported | Active risk concern

How to use this table: Prioritize the section according to your goals. If autoship makes 50%+ of your annual revenue, the recurring billing row should be given more importance to measure setup complexity. If you are already operating in multiple countries, the global expansion section should drive your decision making process. There is no 100% perfect payment. Every choice comes with its pros and cons hence companies should find the right fit that suits their current growth stage, risk and technical capability.

Discover how we build resilient businesses with advanced MLM functionalities

The comparison matrix: Decision factors at a glance

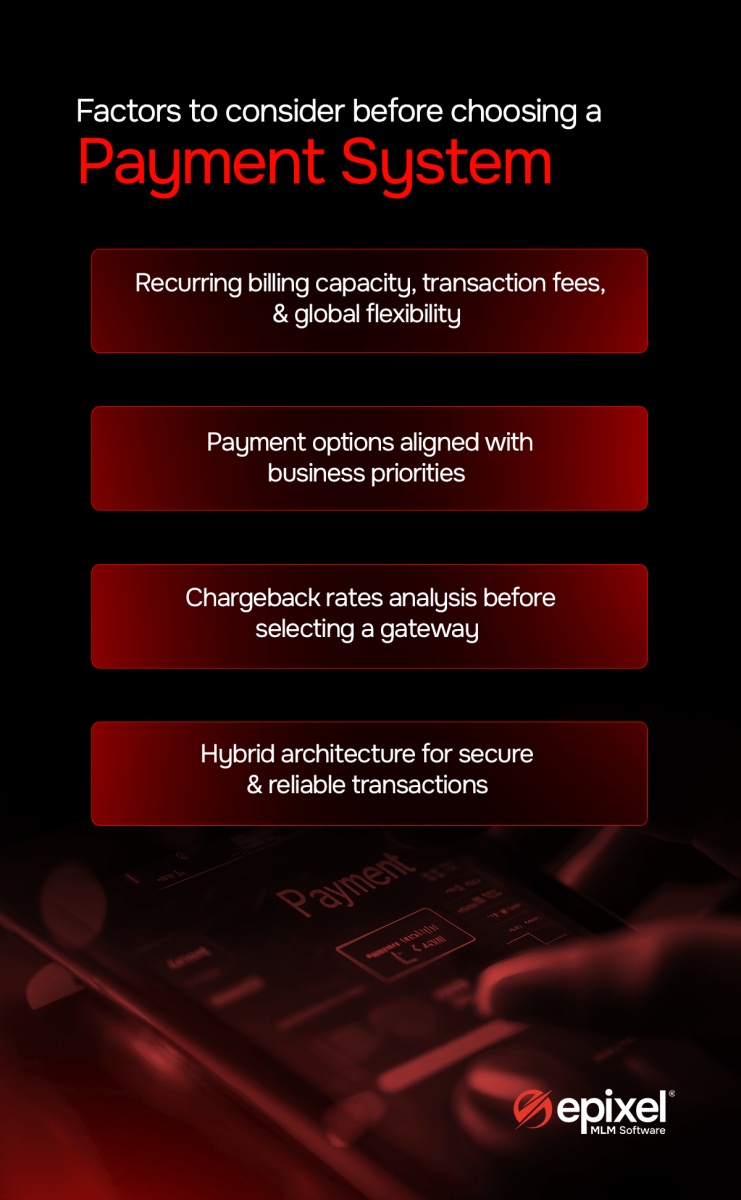

MLM operators consider several factors before they decide upon the payment channel to be used. This includes ease of setup, transaction fees, and cost, recurring billing capability, global flexibility and compliance support.

Stripe is ranked first when it comes to technical flexibility while being moderate in risk management and global capability. Likewise, PayPal is the most trusted option among users while having lesser technical flexibility. The custom system ranks the highest in risk management while low on speed to implement and high operational costs.

The practical recommendation for MLM companies is to invest in a hybrid structure. In early stages of the company, it is recommended to use Stripe as it is easier to set up and has an easy API integration. Use PayPal as a secondary option because it is trustable among the mass and can help with lead generation and conversion in major MLM markets. A careful plan should be drawn out to develop an in-house custom payment system as your company expands into multiple markets.

Key questions for your internal decision process

Before finalizing on the payment gateway, it is essential for your leadership team to ask certain questions. The most important of all is to analyze the chargebacks. If they are above 0.8%, there should be a better system to control it as most payment gateways charge penalties or freeze payments. If autoship is what accounts for a major portion of annual sales revenue, the company should prefer payment gateways that include advanced features for recurring billing. If you see yourself expanding into more than 5 countries, the safe bet is making use of Stripe’s global infrastructure over using PayPal.

The bottom line

Payment gateways can’t be left unmonitored once the installation is complete. A company may require switching from one payment channel to another, as the company expands. A wrong channel can result in freezing payments, facing penalty charges, and damage to brand reputation. The suitable one quietly processes the transaction while the leaders can focus on leading their teams without the worry of payment.

MLM companies choosing their payment gateway shouldn't only consider the feasibility factor. MLM companies have more complex transactions like autoship billing, distributor commissions and more. Hence, a payment gateway should be chosen after analyzing its technical stability and risk management capabilities. Build a payment architecture with the upcoming three to five years in mind. This is because changing the course when the problems arise will cost far more than creating a careful architecture upfront.

Leave your comment

Fill up and remark your valuable comment.