English

- English

- Español

- 简体中文

- Français

- Deutsch

- Italiano

- 日本語

- 한국어

- Portuguese, International

A strategic guide for direct selling leaders in the US, EU, and UAE

KYC and money laundering crimes have entered billions in recent years forcing countries to instate strict AML/KYC laws in place to protect businesses and consumers. Governments and federal agencies in the US, UK, Europe, and UAE have implemented laws and policies to curb AML and KYC-related concerns that affect the economy and systemic balance. AML and KYC processes have become the core of governance strategies to protect revenue and build trust.

European Union in 2025 enforced EU AML Regulation 2025 (AMLR) to be applicable across all member states with a new central authority (AMLA) overseeing the activities. Customer Due Diligence (CDD) and a risk-based approach are to be implemented by companies to keep AML and KYC risks at check. UK AML/KYC regulations come under laws like Money Laundering Regulations 2017 require businesses to verify customer details, assess risks, and apply Customer Due Diligence (CDD) and Enhanced Due Diligence (EDD) for high-risk cases.

The US, through Bank Secrecy Act (BSA), USA Patriot Act, and AMLA 2020 requires companies to complete customers’ KYC process and reporting suspicious activities to FinCEN (Financial Crimes Enforcement Network). The regulatory situation in UAE is not different. Key regulations in the country are Federal Decree Law No. 10 of 2025 and Central Bank of UAE (CBUAE) Regulations supervised by the Financial Intelligence Unit (FIU).

Investors and lenders demand a clean audit as a decision making factor for fund requests. Companies with international financial operations are at a higher risk because weak controls attract legal complications and fines, and delay deals as they strongly impact investor confidence.

Companies who have implemented country-specific and payment-specific screening rules, and continuous customer verification processes have seen reduced alerts related to KYC and AML activities. In fact, these companies expected to see a 60% reduction in false alerts. When this dropped, compliance analysts took lesser time reviewing and freed up more than two full-time employees (FTEs) for every one million payouts processed. So, even with increasing transactions and finance-related activities, companies didn’t have to increase resources. These savings balanced the company’s first-year technology investments in about nine months.

The compliance management process thus turned out to optimize EBITDA, payout speed, and risk control measures of companies.

The international market has seen changing sanctions and new types of identity fraud. Traditional compliance management processes are less competent to detect risks and frauds in real-time international payment systems. Businesses such as direct selling are in higher risk category as they involve large number of payouts, customers, and distributors. The sanction rules also keep changing, and companies must keep up with change to avoid getting listed.

Regional governing bodies update sanction rules frequently, sometimes every week but payouts happen much faster, every minute. Payouts are often processed or can be processed before or during the time a sanction comes into effect. This becomes a serious regulatory concern for companies.

In the US, OFAC issued 50% more Specially Designated Nationals (SDN) updates in 2024 than in 2022. At the same time, in Europe, sanction limits expanded to include crypto asset service providers. Regionally, sanction lists widen to impact industries and individual companies through strict screening and law enforcement.

Timing appears to be the new challenge with sanction lists changing weekly and payment gateways clearing transactions in minutes. If a company does not resort to real-time screening, the risks of getting caught in regulatory sanctions are higher.

AI-powered fraud techniques such as deepfakes are used to impersonate real individuals during onboarding and verification to get through the KYC process. Sumsub’s 2024 Identity Fraud Report revealed that global fraud attempts using deepfakes constitute 7% of total fraud attempts. This is a four-fold increase from 2023 and deeply concerning for companies because this makes it harder to detect fraud using traditional document checks or biometric comparisons.

7% of global identity fraud attempts use AI-powered deepfakes

Sumsub 2024 Identity Fraud Report

As a remedy, AI can boost compliance efficiency of businesses with advanced large-language-model (LLM) matchers that can understand name variations, transliterations, aliases, and contextual risk more than conventional systems. LLM systems can help compliance teams identify more real risks while reviewing fewer suspicious transactions.

LLM models can reduce sanctions-related false positives by 92% and increase real detections by 11%.

Federal Reserve Board's Finance and Economics Discussion Series (FEDS)

It is surprising and equally dangerous that many direct selling companies still stick to monthly or quarterly screening process. It carries larger risk because if a change happens in distributor details or a distributor surface in a sanctions list after the screening process, that risk may go undetected until the next screening period. The payout process may still continue and the company may be charged for sanction breach or fraud.

Perpetual monitoring can reduce this risk with automated processes overseeing KYC and AML checks. But this works only with quality data and fewer false positives otherwise teams get overburdened with false alerts and causes operational delays, taking the process back to point one.

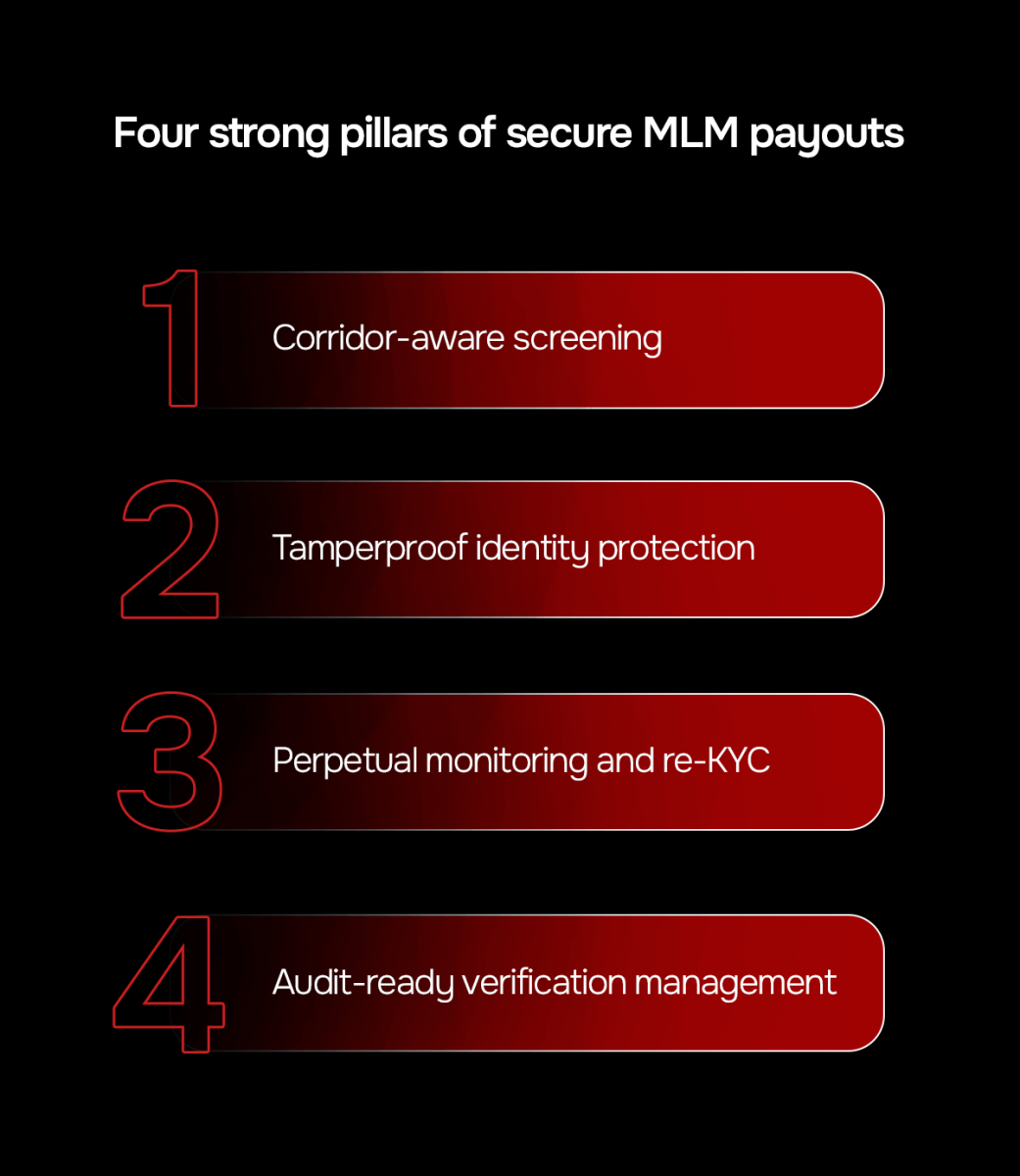

Timely payouts are a trust booster for MLM businesses. But it carries a significant number of risks related to identity frauds and regulations. Companies cannot compromise distributor expectations and operational risks. A balanced approach that takes trust and security together is what businesses need. The four pillar strategy is an approach that takes into consideration the regional policies and limitations to build an audit-ready KYC/AML process.

The screening priorities and intensity for a specific region depends on the frequency of sanctions and enforcement severity. Some regions are stable while others witness frequent sanctions and policy changes.

Corridor-aware screening helps in ranking each payout corridor with a sanctions heatmap based on frequency of changes screening alerts and sanctions lists and indirect sanctions risks. When the ranks are established, companies can set up screening intensities using fuzzy matching and LLM-based similarity models for high risk corridors and lighter, exact matching screening for low risk corridors.

The main motif of this approach is to block synthetic and deepfake identities during onboarding. Identity proofing at this stage should be tamperproof. This strategic pillar relies on tri-modal verification which combines government-issued ID checks, biometric selfie verification, and passive liveness detection to prevent deepfakes.

When these checks are implemented with device and behavioral analytics, it detects emulator usage, clipboard manipulation, or abnormal interactions. A graph analysis is used to identify repeat attackers trying to reuse identity or devices.

The importance of strict monitoring even after a rigorous onboarding process is that distributor details change, and sanctions lists are updated after onboarding process. If these are not updated in the system, it can cause serious trouble for businesses.

Perpetual monitoring ensures that any time a change in behavior or sanctions lists update is detected, distributors are routed through a KYC re-verification process. The re-KYC process is not applied uniformly unless there is a change in situation. But high earning and high risk distributors are re-verified more frequently and low risk distributors are put under a longer re-verification cycle.

When businesses apply strong processes and strict monitoring for AML/KYC-related issues, they should be easily manageable and auditable. Because revisiting an auditing process is not favored by regulators and is not favorable for the company's reputation too.

This pillar focuses on documentation and automation through which every sanctions list version is hashed, every screening decision is recorded, and reports can be exported in regulator-friendly formats such as goAML or AMLA templates.

AI or automated screening tools need to be reviewed regularly to ensure that they are still identifying risks accurately. Companies and their compliance teams must document sanctions list updates and sources for future reference and management.

A simple scorecard can manifest the risks associated with KYC-related processes. The KYC checklist and risk scorecard bring all distributor checks into one centralized location and reveals who has passed sanctions and identity checks, high risk payout routes, and high risk distributors requiring re-verification. The scorecard compiles decisions, settings, and results to help compliance teams work faster and maintain audit-ready reports on KYC verification.

A checklist records KYC and screening results including sanctions, PEP status, adverse media flags, identity and liveness checks, bank and address verification, and device risk indicators.

The risk scorecard assigns a risk score for each payee and segments them into a risk band based on the checklist insights.

Corridor profiles assign a score from 0-10 for each payout corridor based on sanctions change frequency, past false positive and onboarding fraud rates, and document quality.

Controls map converts each risk into action by aligning risk bands with operational controls like payout caps and frequency, re-KYC frequency, and compulsory verification steps.

Audit log records every activity and the same can be exported in preferred formats for review.

Outcomes are displayed in the Results section through automated KPIs, and a dashboard gives leaders an overview of risk distribution, corridor exposure, and effectiveness of controls.

Estimate the ROI for each pay cycle design with a detailed expense analysis with our Pay Cycle ROI Simulator

Many network marketing companies choose to designate third parties for AML/KYC verification process after weighing the costs of allocating an in-house team. When choosing a partner, it is not only about choosing one with an advanced technology framework, but also about guaranteed service standards and legally abiding contracts.

Sanctions screening, payment systems, and KYC processes are more efficient when using single API connectors. It reduces integration debt, standardizes error codes, and speeds up operational workflows.

But if a partner compromises the accuracy, the company will have to face the repercussions. In order to avoid this, accountability must be included as a clause in contracts. Technology is the primary factor when entering a partnership but it takes legal and contractual agreements to protect the business.

Partner agreements have to be locked in with necessary clauses and conditions to ensure that company is safe and the processes are accurate and efficient. Here are five must-include clauses in partner agreements.

Partners must disclose all sanctions and watchlist data sources used like OFAC, EU, UN, and UAE lists. These data must be updated within 24 hours after an official update to ensure screening tests are based on updated regulatory policies. Any deviance to this should be considered as a contract breach.

Partners must provide detailed explanations on the working of the screening model. It should list how screening decisions like match thresholds, name-matching logic, synonym handling, and transliteration rules are made. This way companies can explain the screening results to regulators or auditors whenever needed.

The partner agreement must mention performance expectations and metrics that will be used to guage performance standards. This can include acceptable false-negative rates and limits on alerts requiring manual resolution. These metrics are used to understand the system and to see if it capable of efficiently identifying real risks. When the partner fails to meet the conditions mentioned in the service level agreement, they will be fined or will have to face legal consequences.

Partners should present the necessary reports on screening and decisions whenever the company demands. The reports should be made available in formats preferred by the company or in CSV and PDF.

The system must support local compliance policies, regulations, and reporting requirements. The system should support STR/SAR submissions and adaptable to future region-specific regulatory requests. This will make it easier for MLM companies working across international markets.

Before starting to implement the controls, risks and associated sources need to be identified which will further reveal what type of controls should be in place and the level of severity.

Review 12 months’ payout data to compare payouts with past sanctions and screening alerts across regions. This will reveal the “silent risk” corridors where transaction numbers are high but alert numbers are low, where risks are not avoided but missed.

Create a KYC risk ladder with three levels and define what checks are needed for each stage. These payout limits and automated re-verification have to be linked with the corresponding levels. When these checks come into effect, it has to be conveyed to the network with detailed needs and processes.

Special clauses in KYC and screening partner contracts with expectations, responsibilities, and penalties must be with the consent of partners. Minimum performance expectation and penalties must be mentioned if they fail to maintain performance should be included in the agreement.

The process has to be carried out in two payout corridors first. Then track the time taken by analysts to review alerts or incidents and identify process issues to measure efficiency.

Biometric and device checks can find the identity frauds. The areas with higher risks and where users discontinue during screening should be monitored. User instructions need to be published to reduce issues before complete implementation.

Run simulations with real regulatory requests by collecting all evidence within 48 hours. This will help identify missing logs, unclear records, or improper documentation before a real audit occurs.

Establish the process across all payout corridors. Set up a team with members from finance and compliance teams to review monthly sanctions updates and quarterly model performance.

Monitoring the payout corridors and model efficiency cannot guarantee risk control. Setting critical metrics and monitoring them brings success to the efforts in setting up the model and keeps risks under control.

Screening alerts are warning signs, but they may not always be accurate. False alerts take time and resources, and even a minor oversight can be a missed real alert. Tracking sanctions false positive rate shows how many alerts turn out to be unnecessary. Higher number of false alerts drain analyst’s time and by keeping a check on the time spent on a false positive, companies can see whether screening quality is improving. Even a 30-60% reduction indicates lower operating costs without increasing risks.

This measures the effectiveness of the system in catching real fraud related to identity theft and money laundering activities. When fraud catch rates are high, brand revenue and reputation stay safe. Also, comparing detection results against industry benchmarks confirm the system is strict and effective.

This measures the time duration between a distributor sale and payout. Faster payouts motivate distributors but there are also risks related to refunds and chargebacks. So keeping the time-to-payout rate balanced, that is, not too fast not too slow, is important to keep distributor trust and payout safety.

This oversees the number of audit issues logged are resolved within the first review cycle. A high close rate shows that an efficient system with strict controls, documentation, and management is in place. 95% close rate hints at the readiness of an organization to respond timely to scrutiny.

Keeping risks under control is important for an organization to strengthen the aspects of revenue, reputation, and retention. Distributors’ confidence in the payout system is directly proportional to their loyalty with the company. Hence, containing the risks with strategic measures that balance risk detection, remediation, and operations is crucial to maintain compliance and competitiveness in the international market.

Epixel MLM Software anchored 450+ network marketing companies to success through their business process automation in more than 88 countries. Let Epixel MLM Platform revolutionize your MLM business with 100+ proven features intelligently tuned for small, medium, and large enterprises.

Try our Ultra-modern

Direct Sales Mobile App!!!

Take your business with you. Anytime. Anywhere.

Epixel Enterprises LLC.

300 Delaware Ave STE 210 286,

Wilmington, DE 19801

United States Of America

Solutions

Products

Resources

Get in touch

Epixel Enterprises LLC.

300 Delaware Ave STE 210 286,

Wilmington, DE 19801

United States Of America